by Craig Klugman, Ph.D.

Do you have pre-existing health conditions? Approximately 23 percent of Americans do.

According to the University of Pittsburgh Medical Center, a pre-existing condition is “a medical condition that occurred before a program of health benefits went into effect.” Healthcare.gov defines it as “A health problem, like asthma, diabetes, or cancer, you had before the date that new health coverage starts. Insurance companies can’t refuse to cover treatment for your pre-existing condition or charge you more.” That means if an adult had a childhood disease, that’s a pre-existing condition. The problem with the healthcare.gov definition is that it is dependent on the Affordable Care Act (ACA) remaining intact, an increasingly unlikely scenario.

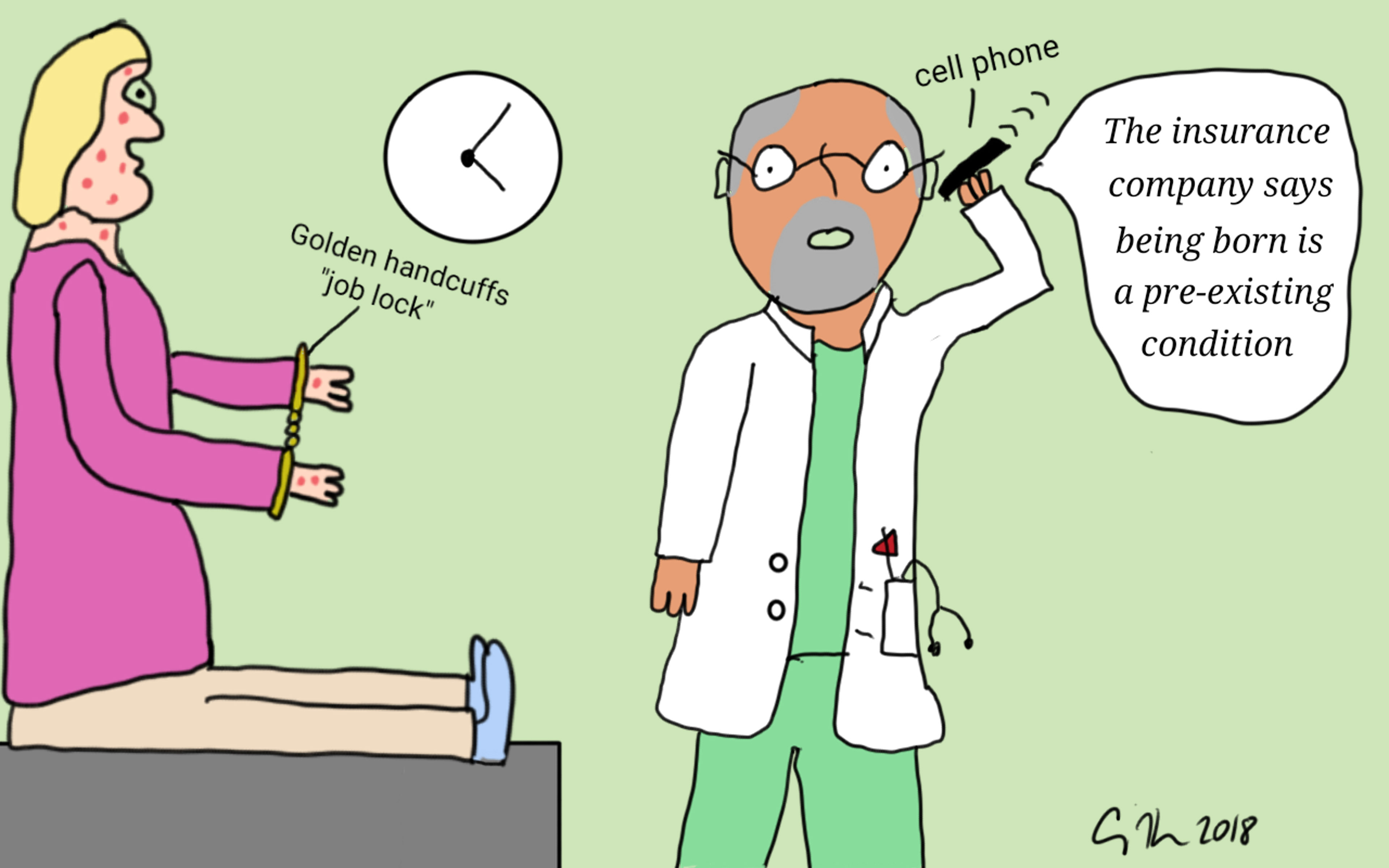

Before the ACA, people with pre-existing conditions could be refused insurance coverage if they moved to a new policy or a new company. This made sense from an actuarial standpoint since a person with a confirmed disease is more likely to need more medical services and thus will cost the insurance company more money. For the insured, this policy meant that they could never change health insurance. If they were diagnosed while covered under a plan, they had to stay with that plan and that insurer to ensure coverage. If one moved to a new job, meaning also a new insurance plan, the insurer might limit benefits related to the condition, might deny any coverage for the condition, might withhold coverage for the condition for the first 6 months to 2 years in the plan, might raise rates for the entire company, or might refuse to cover the employee. A person might even not get job offer because their chronic disease risked raising health insurance costs for the company. This resulted in people with chronic illnesses or with immediate family members with chronic illness being trapped in their jobs, i.e. “job lock”. To leave their position, even to take a better opportunity somewhere else, meant risking needed health insurance coverage. Without the ability to leave a position, people earned less and had to withstand toxic environments. They were trapped.

The Affordable Care Act changed this bizarre situation. Under that law, insurers can no longer refuse or limit coverage (or charge higher rates) to someone because they had a pre-existing health condition. In 2010, the ACA banned using pre-existing exclusions for children, and set up high risk pools to help adults denied insurance. In 2014, the law extended this protection to everyone. This rule is one of the most popular parts of the ACA. A new poll from the Kaiser Family Foundation found that no matter their political affiliation, most Americans are supportive of the ACA pre-existing condition rule. KFF reports that voters are looking at candidate’s position on pre-existing conditions for the November election and that the public is against the US Supreme Court overturning the ACA.

This news is welcome to those of us who support broader access to health care and health care financing, but it goes against the stated positions of the current Administration in Washington DC. In recent months, Trump has proposed two rules, both of which would allow the creation of insurance instruments that bypass the ACA minimum coverage requirements, including coverage for pre-existing conditions.

Twenty states are suing the federal government saying that with the defeat of the individual insurance mandate, the rest of the ACA is also unconstitutional. The Department of Justice is not defending the law. If the states win, then insurers would be free to reinstitute pre-existing condition clauses in coverage. Oddly, nine of the states in the suit have the highest rate of adults with preexisting conditions in the country.

The lawsuit comes after several Congressional bills attempted to rollback the ACA. Under the Cassidy-Graham bill, states could have opted-out of ACA regulations, including requiring insurers to cover pre-existing conditions. The also defeated American Health Care Act would have allowed restrictions on coverage for pre-existing conditions for any person who had a 63-day gap or more in health insurance coverage

This is a uniquely American situation. As a matter of policy, the U.S. holds health insurance and health care services to be a privilege, not a right. And it is a privilege that no one has an obligation to provide. With job lock, changing jobs was about more than a satisfying set of duties, money, and challenges—it also included what type of health insurance coverage a person and their family would have. The ACA freed a lot of people from job lock. Sadly, we may soon be moving back to this situation given Administration statements and the 20-state lawsuit. Given the popularity of the ACA pre-existing condition rule, hopefully all of those people will let their elected officials know of their support through letters and phone calls (email, petitions, social media posts, and polls are less influential). The hope in preventing a rollback of this protection lies in lobbying for a defeat of these efforts and in voting in November.